Risk-Managed Strategies

A smoother ride to long-term capital appreciation

MarketGrader Capital’s Risk-Managed Strategies seek to provide accredited investors exposure to our intelligent, fundamentals-driven equity indexes with a tactical risk management overlay that aims to minimize the negative impact of bear market events on long-term capital appreciation. Designed to track the rules-based MarketGrader Risk-Managed Indexes, the Strategies utilize a separately managed account (SMA) structure to provide maximum transparency to family office and institutional clients.

Created in partnership with risk management specialist Kaizen Advisory, the Strategies are desirable for investors seeking to capture the performance of the most fundamentally sound quality companies selected by MarketGrader's growth at a reasonable price (GARP) methodology while managing the large drawdowns and associated volatility inherent in the equity asset class.

- Diversified Smart Beta Equity Exposure

- Fundamentals-Driven GARP Stock Selection

- Tactical, Rules-Based Risk Management Process

- Lower Cost and Efficient Hedging Methodology

- Transparency of SMA Structure and Replicable, Published Indexes

- Enhanced Risk-Adjusted Returns Over Market Cycles

Download U.S. Risk-Managed Strategies Document

Download U.S. Risk-Managed Strategies Document

The Risk Management Process

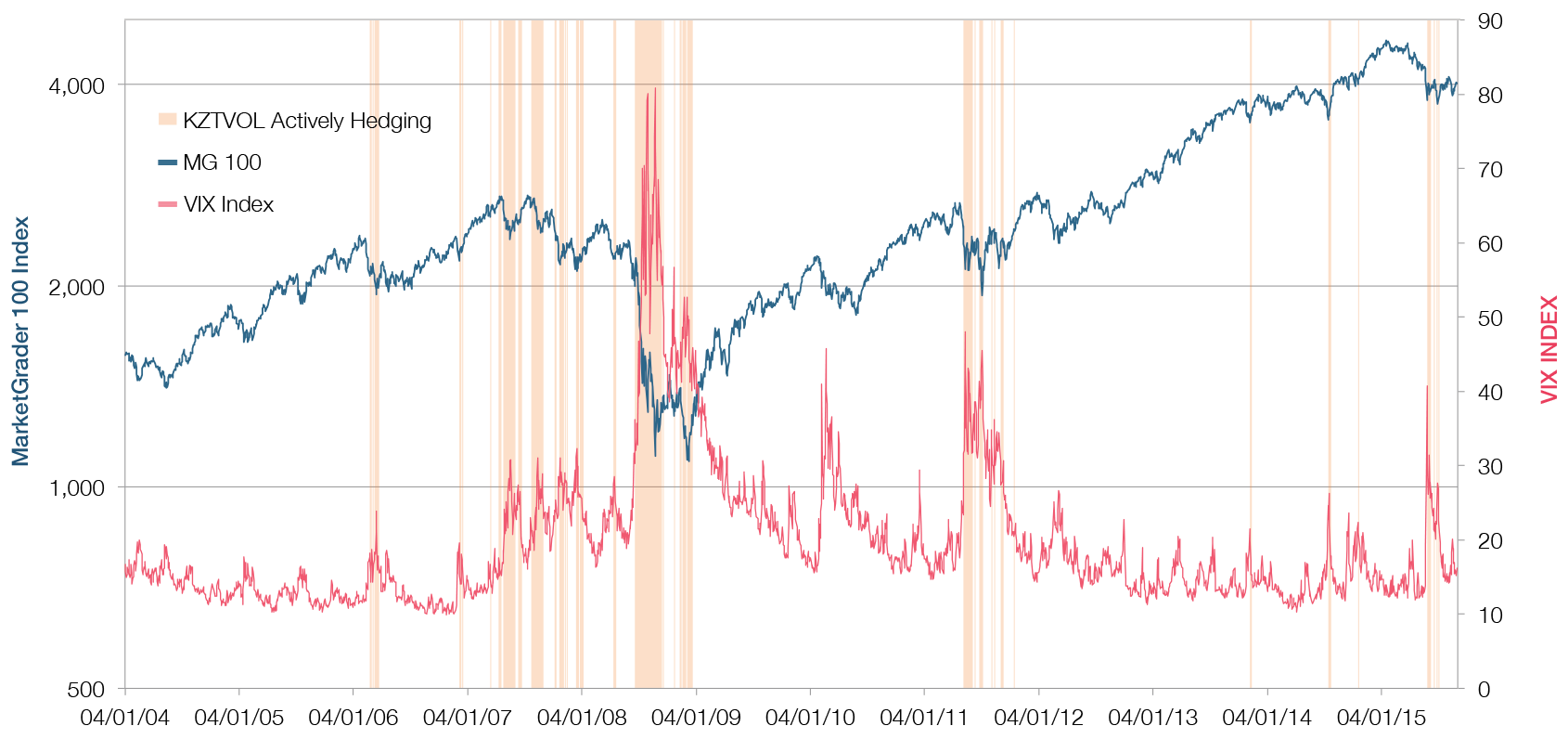

The MG Risk-Managed Index series combines MarketGrader's core country indexes in select large equity markets with a tactical risk overlay from Kaizen Advisory. Portfolio Managers Michael Thompson, CIO, CFA, and Matt Thompson, Director of Research, CFA, designed the Kaizen Dynamic Risk Overlay Index (KZTVOL) to be a rules-based, lower cost and more effective hedging solution than the ubiquitous and expensive options-based methods applied constantly or at the discretion of the manager. This proprietary process is the culmination of the Thompson brothers’ combined 30+ years innovating in the field of risk management and derivatives trading, particularly in the service of large insurers.

The Kaizen Dynamic Risk Overlay behaves like catastrophe insurance for the underlying MG Index in times of systemic events, providing a payout when equities face sustained and significant selling pressure.

Utilizing a rules-based hedging technique that is automatically triggered under certain conditions common to past systemic events, the Overlay is governed by market volatility, using the VIX and associated measures of stress to gauge the drawdown potential in equities. When the hedge signal is on, the given MG Risk-Managed Index allocates 30% to certain VIX futures contracts. In times of market stress, VIX futures increase in price as participants rush to hedge risk, typically providing uncorrelated returns with equities.

The Overlay never sells or shorts the selected underlying MG Index; it is always long equities. This decreases risks associated with other hedging techniques. As measured by price returns on the VIX futures, the Overlay signal provides a positive return in roughly half the instances the hedge is applied. The performance drag on the given MG Risk-Managed Index of a hedge placed when VIX futures prices drop is a fraction of the positive contribution when VIX futures rise.

This replicable and systematic process delivers an effective hedge that is only applied tactically. Based on historical conditions since the April 2004 inception of the backtested results, the hedge has been activated 5% of trading days and about one quarter of months on an annualized basis.Under normal market conditions, the hedge is not activated, allowing the proven strength of MarketGrader’s GARP stock selection methodology to fully drive performance.

The rules-based hedging process is demonstrated below using the MG 100 Risk-Managed Index. Instances when the signal is on, causing the Index to allocate to select VIX futures contracts (long volatility), are shaded. As is seen, the hedge is typically triggered when spikes in the VIX occur. Elevated VIX levels represent expectations of heightened volatility and potential pressure on equities.

The construction of the MG Risk-Managed Indexes tracked by the Strategies has the potential effect of decreasing drawdowns, while the tactical nature of the hedge allows the fundamentally-sound quality companies selected by the proprietary GARP methodology to generate significant upside participation in normal market conditions. Over market cycles, this unique combination typically results in an improved risk/return profile for investors.

For more information on MarketGrader Risk-Managed Index Series, including the MG 100 Risk-Managed Index, please visit https://www.marketgrader.com/indexes/riskManagedIndexes

Invest with us

For more information about the MarketGrader Risk-Managed Strategies, please write us at info@marketgradercapital.com.